Introduction to Personal Finance

Introduction to Personal Finance

Presented by: Michael Sayre, CPFA™, AIF®

Goals of This Module

Define personal finance.

See what the average American’s finances look like.

Learn about common behavioral finance biases and fallacies.

Distinguish between needs, wants, and wishes.

What is Personal Finance?

One of the basic concepts of economics is that we live in a world of scarcity. Because of this, we need to learn to manage our resources efficiently. Poor management can lead to unnecessary debts, stress, and dependency on others. On the other hand, skillful money management can help you accomplish goals and live a fulfilling life.

Personal finance refers to managing an individual's or a household's financial resources, including income, expenses, savings, investments, and debt. It involves making informed decisions and taking actions to achieve financial goals and effectively handle money matters. Personal finance encompasses many aspects of one's economic life. The primary aim of personal finance is to achieve financial stability, security, and long-term financial well-being by making wise financial choices and managing resources efficiently.

How Do Americans Manage Their Finances?

Now that you know what personal finances encompass, how well does the average American manage them? Here are a few financial facts about the average American’s finances.

Credit Card Debt

The average American has $5,733 in credit card debt(1).

The average credit card interest rate is 28.06% (2)

Average Retirement Account Balance

The average retirement account balance in America is $95,776 (3)

Financial Stress

70% of Americans are feeling financially stressed (4)

Available Income

Over 60% of Americans live paycheck to paycheck (5)

The average American's finances can provide a valuable perspective on our financial situation. It allows us to gauge where we stand with the broader population. This perspective helps us benchmark our situations and recognize areas of strength and weakness.

Behavioral Finance

Behavioral finance incorporates insights from psychology and economics. It aims to understand how individuals and investors make financial decisions. Traditional finance theory assumes that people are rational and always make decisions that maximize their utility or wealth. However, behavioral finance challenges this assumption by recognizing cognitive biases, emotions, and heuristics (mental shortcuts) can lead to irrational decision-making in financial matters. Here is a list of expected behaviors and tendencies.

Herding Behavior

Investors often follow the crowd, even when it may not be rational. This behavior can lead to groupthink and the fear of missing out, leading to market bubbles and crashes.

Risk Aversion

People tend to choose options with known outcomes or lower perceived risk to avoid the possibility of losses, even if riskier options offer higher expected returns.

Winner’s Curse

This phenomenon occurs when an investor pays more for an investment than it is worth by outbidding others due to a lack of awareness of its intrinsic value.

Loss Aversion

Loss aversion bias is a psychological phenomenon and cognitive bias. It explains the tendency to strongly prefer avoiding losses over acquiring equivalent gains.

Mental Accounting

People tend to categorize and treat money differently based on the source of income or the intended purpose of the funds.

Hindsight Bias

A cognitive bias refers to people's tendency to perceive events as having been more predictable after they have already occurred than before.

Anchoring

This bias occurs when individuals rely too much on the first information encountered when making decisions.

Confirmation Bias

People are inclined to pursue, interpret, and remember information in a way that confirms their preexisting beliefs while ignoring contradictory evidence.

The Gambler's Fallacy

A belief that future random events are influenced by past events in a way that balances previous outcomes, even when there is no logical reason for such an influence.

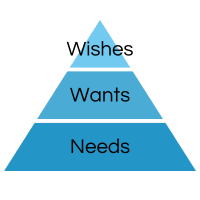

Personal Finance Prioritization

When it comes to personal finance, understanding the difference between wishes, wants, and needs is crucial. It can be challenging to distinguish between these three categories. Each category represents a different level of importance and urgency, and identifying which expenses fall into which category can significantly impact our financial decisions and overall well-being. Let's delve into the distinctions between wishes, wants, and needs and how they relate to personal finance.

Wishes

Wishes, also known as dreams or aspirations, encompass those desires that may seem enticing but are not essential for survival or well-being. We often daydream about these things, like luxury vacations, gadgets, or extravagant purchases. While fulfilling our wishes can bring temporary joy and satisfaction, they are typically non-essential items or experiences we could live without.

Regarding wishes, it's essential to approach them with caution. While aspirations are natural, spending a significant portion of our finances on fulfilling wishes can impair our long-term financial stability. Considering our overall financial health and goals before indulging in wishes is essential, ensuring we have a strong foundation before pursuing these desires.

Wants

Wants fall somewhere between wishes and needs on personal finance. They are desires we can live without but are considered closer to our daily priorities and have a higher level of importance. Wants often involve purchases that enhance our lifestyle or provide us with a greater level of comfort and convenience.

Examples of wants might include:

Dining out at restaurants regularly.

Buying mid-range electronics.

Upgrading to a newer car model.

While fulfilling these wants can enhance our quality of life, it's essential to approach them with a sense of balance. Overspending on desires without considering their long-term impact can lead to financial strain and potentially hinder our ability to meet future needs.

Needs

Needs represent those expenses that are fundamental to our survival and well-being. These are the essential items and services required to maintain a basic living standard. Basic needs include shelter, food, clothing, transportation, healthcare, and education.

Differentiating needs and wants can sometimes be challenging, as wants can disguise themselves as needs. However, understanding that needs are vital for survival can help us prioritize our spending. Focusing on meeting our needs before indulging in wants or wishes is essential. By securing our basic needs, we provide a stable foundation to build a healthier financial future.

Balancing the Three

Finding a balance between wishes, wants, and needs is critical to maintaining financial stability and achieving our long-term goals. While it's natural to have desires and aspirations, it's essential to ensure that we prioritize our needs and make conscious decisions regarding our wants and wishes.

Developing a budget and financial plan can help us allocate our resources appropriately and provide a roadmap to navigate our economic aspirations. By reviewing our financial goals regularly and assessing our spending patterns, we can better differentiate between wishes, wants, and needs and make informed financial decisions.

Distinguishing between wishes, wants, and needs is essential to personal finance. While it's natural to have dreams and desires, it's crucial to prioritize our needs and make conscious decisions regarding our wants. Balancing these three elements is critical to maintaining financial stability, securing our basic needs, and working toward our long-term financial goals. As always, your financial advisor team is here to help.

Action Items

Review the behavioral finance biases listed in this section.

Be aware of behavioral financial biases as you make financial decisions.

Review your spending habits and categorize expenses and spending as needs, wants, and wishes.

1. (https://www.fool.com/the-ascent/research/average-household-debt/#:~:text=According%20to%20TransUnion%2C%20Americans%20had,average%20of%20%241%2C110%2C%20per%20Experian.)

2. https://www.forbes.com/advisor/credit-cards/average-credit-card-interest-rate/

3. https://www.forbes.com/sites/andrewrosen/2023/03/02/how-your-retirement-savings-compare-to-the-national-average/?sh=73b66f9e6b2a

4. https://www.cnbc.com/2023/04/11/70percent-of-americans-feel-financially-stressed-new-cnbc-survey-finds.html

5. https://www.cbsnews.com/news/paycheck-to-paycheck-6-in-10-americans-lendingclub/